· deepdives · 8 min read

Payment Request API vs. Traditional Payment Methods: The Future of Online Transactions

A practical comparison of the Payment Request API and traditional payment flows - covering UX, security, browser support, implementation steps and illustrative case studies to help businesses decide whether to adopt the API now.

Outcome-first: read this and you’ll know whether the Payment Request API can raise conversions, simplify PCI scope, and speed checkout for your customers - and how to implement it with safe fallbacks.

Why this matters. Slow, clunky checkouts cost revenue. Faster, frictionless payments convert better. The Payment Request API promises one-click-like payments across browsers and devices. But it’s not a silver bullet. This article walks you through strengths, weaknesses, real-world integration patterns, and a clear decision framework so you can act with confidence.

Quick primer: how “traditional” online payments work

Traditional payment flows on the web usually look like this:

- Customer fills out a multi-field checkout form (name, address, card number, expiry, CVV).

- The browser sends data to your server, which forwards it to a payment gateway (Stripe, Braintree, Adyen, etc.).

- The gateway tokenizes the card and processes the authorization.

- Merchant handles shipping, fulfillment, receipts, and reconciliation.

This model works. It’s proven. But it has downsides: long forms, high abandonment rates, and, depending on the integration, a large PCI scope.

Readability check: that friction kills conversions. Short forms win.

What is the Payment Request API? (short)

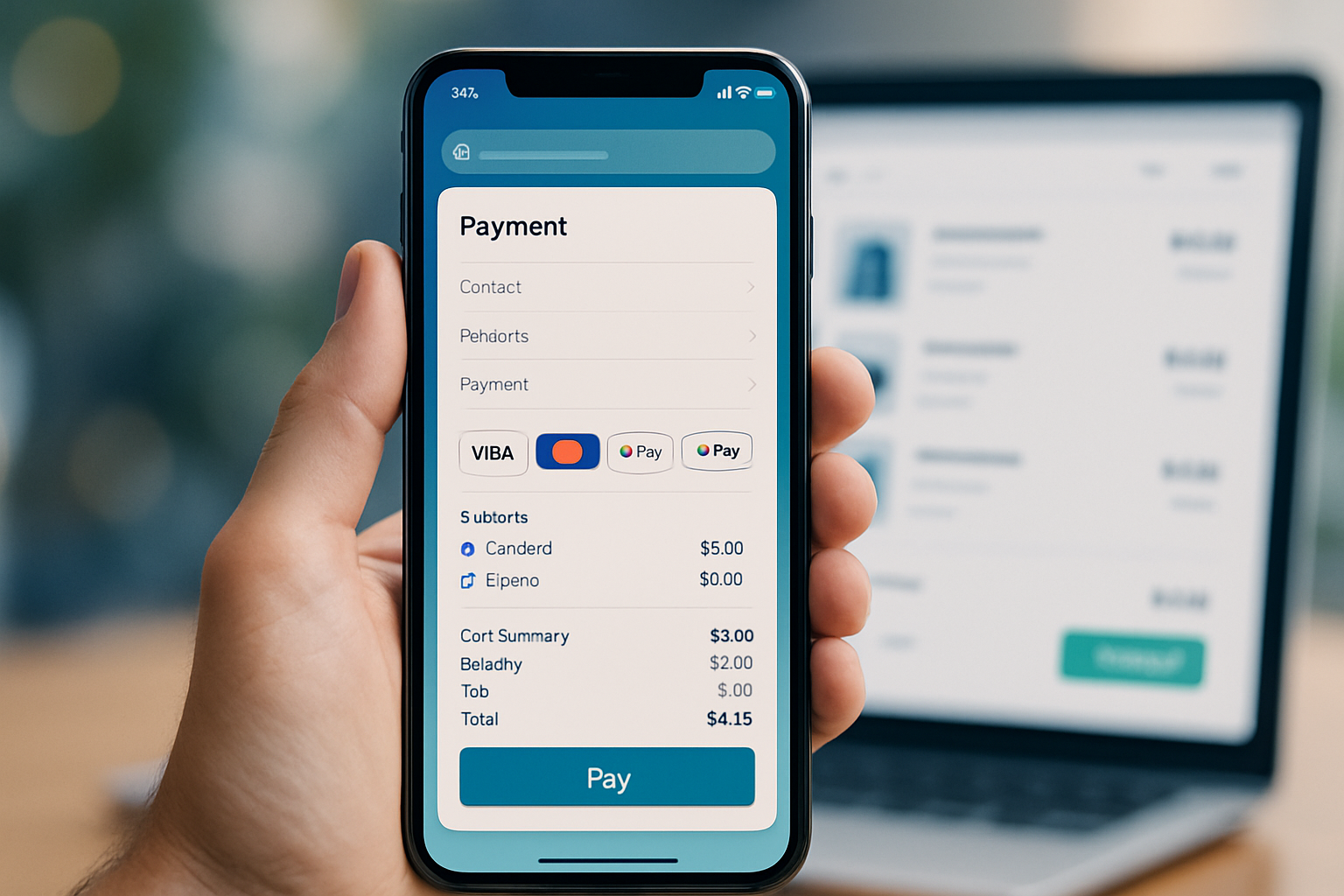

The Payment Request API is a browser standard that lets merchants request payment from a user with a single, consistent UI provided by the browser or a platform wallet (Google Pay, Microsoft Pay, etc.). Instead of building and validating a long form, the browser shows the user’s stored payment methods, shipping options, and address autofill, and returns a tokenized payment response to the merchant.

See the specification and compatibility notes here: https://developer.mozilla.org/en-US/docs/Web/API/Payment_Request_API and https://www.w3.org/TR/payment-request/.

Strengths of the Payment Request API

- Better UX - native, consistent checkout UI reduces friction and cognitive load. People don’t like typing long forms on mobile. The API surfaces saved cards and native wallets (Google Pay, Microsoft Pay) so checkout can be one tap.

- Faster time-to-checkout - fewer fields and built-in validation mean quicker completion and fewer errors.

- Reduced keyboard friction on mobile - the browser surfaces appropriate input methods and saved credentials.

- Tokenization-friendly - the API returns payment method tokens (when used with a gateway), which reduces merchant exposure to raw card data.

- Integrates with platform wallets - works with Google Pay, and with some gateways (Stripe, Adyen) for a unified UX.

- Consistent developer API - browser provides a single JS API instead of numerous SDKs for each wallet.

Google has published guidance on improved checkout UX and adoption patterns: https://developers.google.com/web/fundamentals/payments.

Weaknesses and limitations

- Browser support is uneven. Not all browsers and device combinations provide the same wallet availability or features. Use the compatibility table on MDN before relying on it: https://developer.mozilla.org/en-US/docs/Web/API/Payment_Request_API#browser_compatibility.

- Wallet coverage varies. Apple Pay has historically used its own JS API in Safari; Payment Request API support for Apple Pay is limited depending on platform and vendor.

- User adoption of stored payments varies by market and demographic.

- Customization is limited. The browser controls the UI - great for consistency, bad for brand-first experiences.

- Advanced flows (complex subscriptions, custom split-payments, certain fraud checks) may still require server-side or gateway-specific logic.

- Analytics and instrumentation may require extra work to capture granular checkout events.

Business case: why switch (or at least test)

- Conversion lift: reducing friction correlates strongly with higher conversion. Research on checkout usability (Baymard Institute) shows large gains from simplified checkout flows: https://baymard.com/research/checkout-usability.

- Faster mobile checkout: mobile is the dominant channel for many merchants; Payment Request improves mobile UX significantly.

- Lower error rates: built-in validation and autofill cut typographical errors and address mistakes.

- Reduced PCI scope where used with tokenizing gateways: when you accept payment tokens directly (for example via gateway Elements or hosted tokenization endpoints), you avoid handling raw PANs. Check your gateway’s guidance and PCI SSC documentation: https://www.pcisecuritystandards.org.

- Lower maintenance overhead: fewer custom checkout widgets to maintain across browsers and devices.

Bottom line: if you rely on mobile traffic and care about conversion, A/B test Payment Request as part of a checkout optimization program.

Implementation checklist

- Inventory payment methods you support (cards, wallets, local methods) and how they map to what the API surfaces.

- Confirm browser and platform coverage for your target audience (use analytics to see browsers and OS distribution).

- Choose an approach:

- Payment Request + gateway integration (recommended for most): use the gateway’s tokenization and server-side processing.

- Payment Request directly with the Payment Instrument (when supported by the platform wallet).

- Implement a graceful fallback: detect Payment Request availability and fall back to your existing form.

- Instrument key events: show, abort, userAccept, response time, and conversion metrics.

- Test edge cases: shipping changes, currency conversions, multi-step flows, and decline paths.

- Monitor security and compliance: ensure tokens are handled correctly and check your PCI responsibilities with your gateway.

Minimal example (client-side)

This simplified snippet shows the general shape of calling the Payment Request API on the client. It omits gateway-specific token exchange and server handling for brevity.

// Basic Payment Request usage (simplified)

if (window.PaymentRequest) {

const supportedInstruments = [

{

supportedMethods: 'basic-card',

data: { supportedNetworks: ['visa', 'mastercard', 'amex'] },

},

];

const details = {

total: { label: 'Total', amount: { currency: 'USD', value: '29.99' } },

displayItems: [

{ label: 'T-shirt', amount: { currency: 'USD', value: '29.99' } },

],

};

const request = new PaymentRequest(supportedInstruments, details);

request

.show()

.then(paymentResponse => {

// send paymentResponse.details (token or card data) to your server

return fetch('/pay', {

method: 'POST',

headers: { 'Content-Type': 'application/json' },

body: JSON.stringify(paymentResponse),

})

.then(serverResp => {

// on success:

paymentResponse.complete('success');

})

.catch(err => {

paymentResponse.complete('fail');

});

})

.catch(err => {

// user cancelled or API not available

console.log('PaymentRequest failed:', err);

});

}Notes:

- In production you should not send raw card PANs to your server; instead use the gateway’s recommended tokenization flow.

- Most gateways (Stripe, Adyen, Braintree) provide guides on how to connect Payment Request to their tokenization endpoints.

See Stripe’s documentation for connecting Payment Request with Stripe: https://stripe.com/docs/stripe-js/elements/payment-request-button.

Fallback patterns

- Feature detect: if

window.PaymentRequestis missing or the offered methods you need aren’t supported, show your existing checkout form. - Progressive enhancement: add Payment Request as an alternative checkout option (“Pay with saved cards / Google Pay”), not as the only path.

- Offer browser-native wallets directly where Payment Request coverage is missing (for example Apple Pay integration in Safari using Apple Pay JS).

Security & compliance considerations

- Payment Request itself doesn’t remove responsibility for PCI compliance. It can, however, simplify your scope if you only receive tokenized payment instruments from a PCI-compliant gateway.

- Always follow your gateway’s recommended integration pattern and consult PCI SSC guidance: https://www.pcisecuritystandards.org.

- Implement robust server-side validation and monitoring for suspicious patterns - easier fraud checks are still required after tokenization.

Instrumentation & analytics

Track these events to assess impact:

- Payment Request shown

- User accepted/aborted

- Response latency (time between show and completion)

- Conversion (completed payment)

- Failure reasons (declines, cancellations, errors)

Collecting these metrics will show whether Payment Request reduces abandonment and increases revenue for your audience.

Case studies (illustrative and real-world context)

Example A - Anonymized e‑commerce merchant (composite)

- Situation: heavy mobile traffic, cart abandonment above 70%.

- Change: implemented Payment Request API wired to a gateway for tokenization, left legacy checkout as fallback.

- Result: mobile checkout completion improved significantly; abandonment dropped by a double-digit percentage during the test window. Instrumentation showed shorter time-to-pay and fewer address-edit errors.

- Takeaway: mobile-first merchants often see the largest relative gains.

Example B - SaaS vendor (composite)

- Situation: friction around paid trial upgrades; customers were dropping off at the payment form.

- Change: added a Payment Request “one-tap” option for returning users with saved cards; used gateway tokenization for recurring billing.

- Result: faster upgrades and higher conversion for returning users; subscription churn unaffected.

- Takeaway: Payment Request is particularly effective for returning customers with stored instruments.

Real-world resources and published guidance

- Stripe offers step-by-step guides and examples on how to use the Payment Request Button with its platform: https://stripe.com/docs/stripe-js/elements/payment-request-button

- Google’s developer guide explains the benefits and best practices for the Web Payments ecosystem: https://developers.google.com/web/fundamentals/payments

Note: many vendors publish anonymized case studies describing conversion improvements; exact impact varies by business, region, and user base.

Decision framework - should your business adopt Payment Request API now?

Ask these questions:

- What percentage of your traffic is mobile? If high, prioritize testing the API.

- Do your customers commonly have saved cards or use platform wallets? If yes, you’ll get greater benefit.

- Can your gateway support tokenization with Payment Request? If yes, easier integration and lower PCI scope.

- Is a branded checkout critical for your conversion and trust? If brand control is essential, you may prefer to combine Payment Request with a branded modal and fallback.

If you answered yes to 1–3: run an A/B test. Start small, measure, then roll out.

Practical rollout plan (90-day sprint)

- Week 1–2: Audit payment methods, browser telemetry, and gateway capabilities.

- Week 3–4: Implement a prototype Payment Request flow in non-production; wire to a test gateway tokenization endpoint.

- Week 5–6: Lab and device testing (mobile, desktops, various browsers), edge cases.

- Week 7–10: A/B test vs. current checkout on a portion of traffic. Measure conversion, abandonment, and error rates.

- Week 11–12: Analyze results, iterate on handling of declines/fallbacks, and plan rollout.

Final verdict

The Payment Request API is not a replacement for all traditional payment logic, but it is a powerful, low-friction tool you should test if your audience includes mobile users and returning customers with stored payment instruments. When paired with a tokenizing gateway and proper fallbacks, it can raise conversions, simplify the user experience, and reduce engineering maintenance. Start small, instrument carefully, and let measured outcomes guide a staged rollout.

References

- MDN - Payment Request API: https://developer.mozilla.org/en-US/docs/Web/API/Payment_Request_API

- W3C - Payment Request API Spec: https://www.w3.org/TR/payment-request/

- Google Developers - Web Payments: https://developers.google.com/web/fundamentals/payments

- Stripe - Payment Request Button docs: https://stripe.com/docs/stripe-js/elements/payment-request-button

- Baymard Institute - Checkout Usability Research: https://baymard.com/research/checkout-usability

- PCI Security Standards Council: https://www.pcisecuritystandards.org